2 months ago

15349

2 months ago

15349

Every crypto holder is frustrated that to spend crypto in the real world, they have to give up custody first, sell on an exchange, wait for settlement, or load a card.

Custodial risk arises when users give up control of their funds to third-party platforms, making them vulnerable to mismanagement, hacks, or insolvency. If custody fails, users lose control of their funds.

Oobit is a global payments solution enabling users to spend their non-custodial cryptocurrencies at millions of Visa outlets globally. In this article, we review Oobit products and compare how it stacks up against legacy systems and other crypto payment solutions in the market.

The custody problem: Why spending crypto still means giving up control

Crypto was built for self-sovereignty, but spending it requires trusting a third party, often resulting in transaction delays and extra fees.

Current crypto card models do not support non-custodial spending. Users must deposit funds into a custodial account, which is prone to custodial risk such as data leaks or security breaches. Take, for instance, the $1.5B Bybit security breach in 2025.

Some of these cards also require that merchants set up new payment rails that support the cards.

Oobit approaches crypto spending differently, providing a non-custodial crypto payments infrastructure for both individuals and businesses. With Oobit, users can transfer value instantly with no conversion delay to Visa outlets, local payment rails, or banks globally.

For businesses, it enables micro-payments at a flat fee, a feature not available on legacy payment systems.

What is Oobit?

Oobit is a global payments application backed by Tether, the company behind the USDT stablecoin. Tether invested $25 million in Series A funding with participation from Solana co-founder Anatoly Yakovenko, CMCC Global, and 468 Capital.

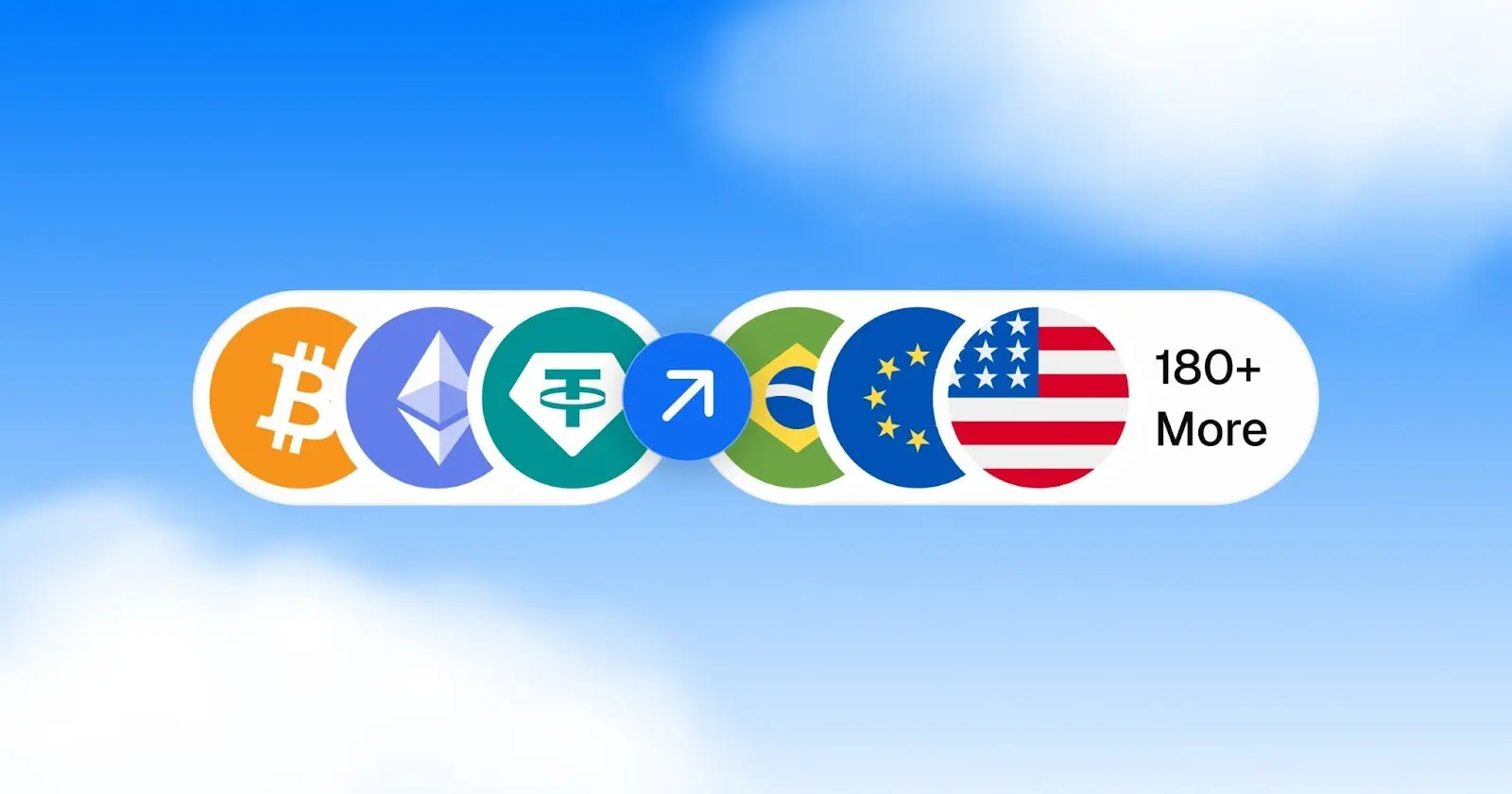

Oobit was established in 2017 and has its headquarters in Singapore. It enables users to spend their crypto at Visa outlets, whether physical or online. The platform also facilitates cross-border transactions in over 150 countries with near-zero fees.

The Oobit Crypto Card is gaining significant traction and already has a 4.8-star rating on the Apple store with 22K+ reviews, and a 4.7-star rating on the Google Play store with 25K+ customer reviews. Also, unlike most crypto debit cards, Oobit has no creation, annual, or holding fees.

Oobit connects your non-custodial crypto wallet with over 150 million Visa merchants globally. You are, however, required to complete Know-Your-Customer (KYC) verification to activate the card.

Non-custodial crypto wallets allow users to hold their own private keys, ensuring full ownership and control over their digital assets without third-party intermediaries.

How non-custodial spending actually works

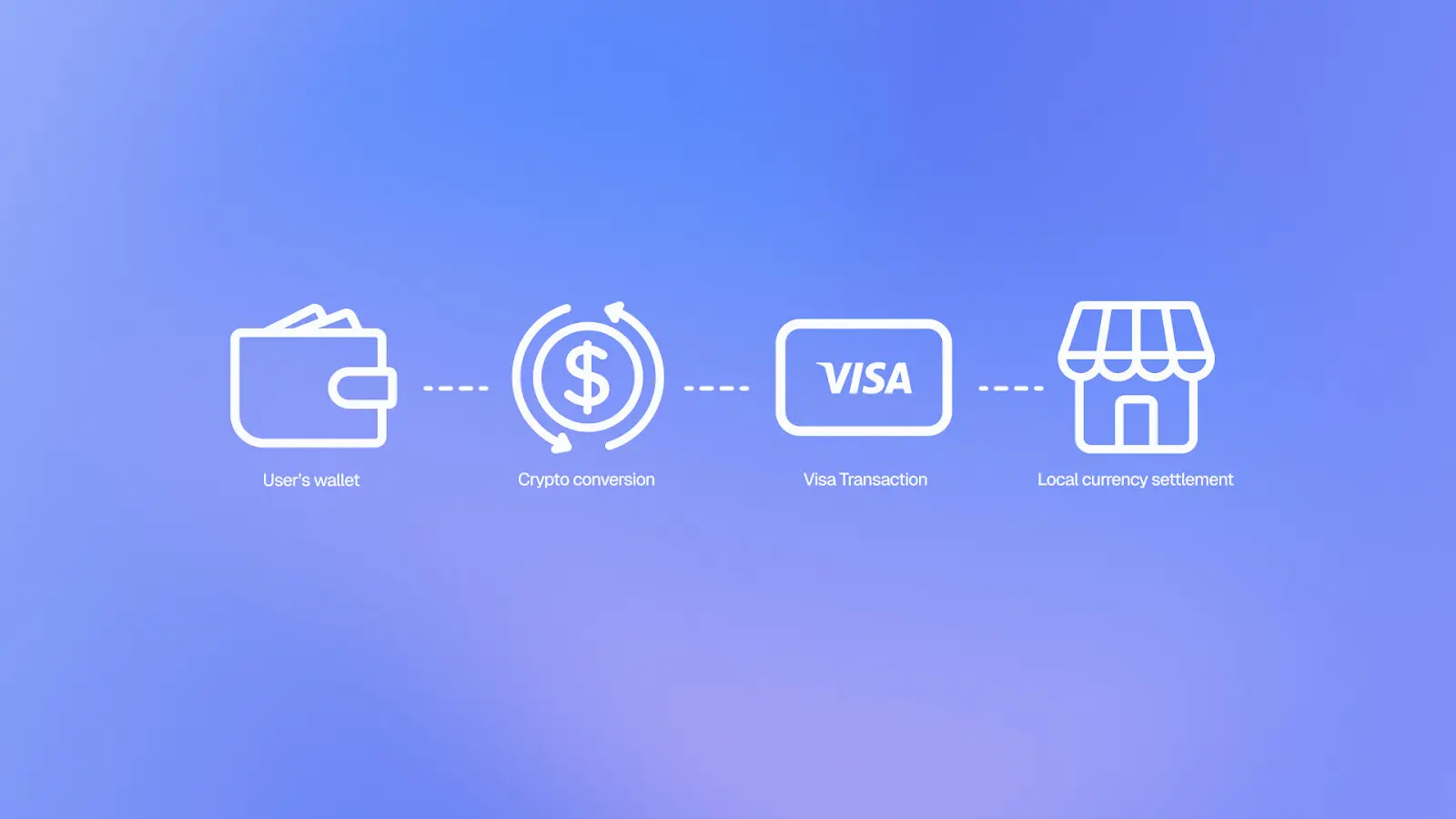

Oobit uses proprietary decentralized payment infrastructure, DePay, to power non-custodial spending with the application.

With DePay, there is no prefunding; users are not required to transfer funds to Oobit, which could introduce custody risks. At checkout, DePay smart contracts execute just-in-time (JIT) token transfers and atomic swaps, enabling instant payments.

Transactions on Oobit are gasless, meaning you do not pay blockchain fees for transactions.

Your crypto wallet keys are never shared with the merchant. Oobit completes the transaction in fiat. No merchant integration; it automatically works with Visa.

Supported blockchain networks include Ethereum, Tron, Binance Smart Chain, Solana, and Polygon.

DePay’s design allows it to be wallet-agnostic, meaning it can work with any Web3 wallet. This is unlike other competitors, who simply wrap a custodial exchange in a card. With Oobit, the user remains on-chain the entire time.

Supported crypto wallets include Metamask, OKX wallet, Binance Web3 wallet, Trust Wallet, Phantom, among others.

Here is a step-by-step procedure for setting up your Oobit application:

- Download the Oobit application.

The Oobit app is available on the App Store for iPhones and Google Play for Android devices.

- Complete Know-Your-Customer (KYC) verification.

The application will then require you to complete KYC verification. This is important to prevent financial crimes such as money laundering, fraud, and terrorist financing. KYC also ensures compliance with local regulations.

Oobit has partnered with Sumsub for a seamless KYC verification. Verification involves the submission of identification documents (identity card, passport), personal details, and passing a liveness check (face match).

- Link your self-custody wallet or fund your Oobit wallet.

At setup, you can choose to create a built-in crypto wallet on Oobit.

The other option is to link your self-custody wallet (MetaMask, Trust Wallet, Phantom, Binance Wallet), so you can start spending, sending, and receiving crypto right away.

You can also purchase crypto worth as little as $10 using a credit card in-app to fund your wallet.

- Add your card to Apple Pay or Google Pay.

This step adds the convenience of wireless contactless payments by replacing physical card swipes. Apple and Google Pay are widely accepted at most stores that offer contactless payment terminals.

- Pay at any Visa outlet worldwide

Use Oobit to pay at any of the 150 million Visa outlets globally. Eligible purchases earn up to 10% cashback instantly.

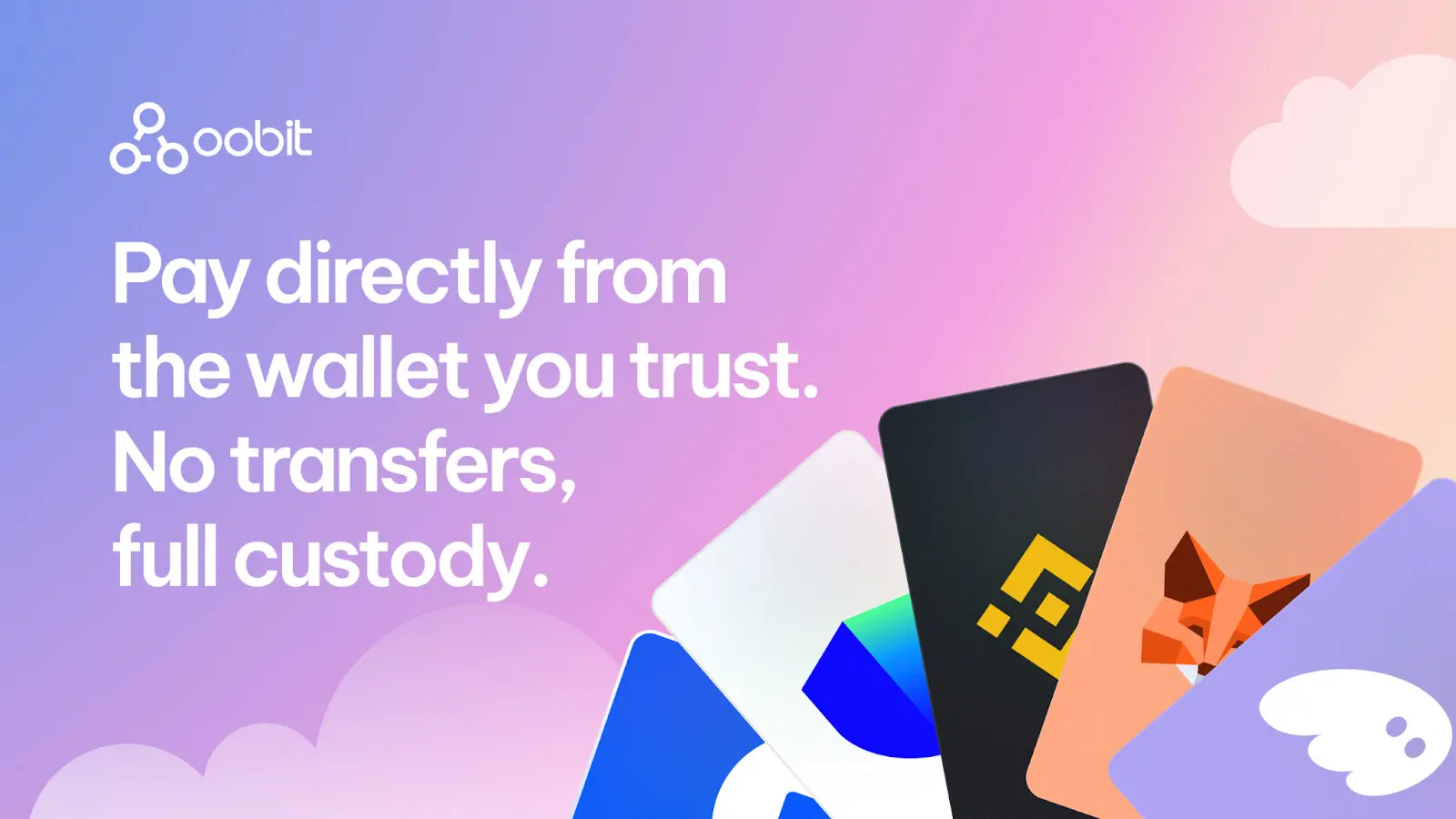

External wallet connectivity. Spend from the wallet you already use

Oobit lets you use your trusted crypto wallets to fund purchases, giving you complete control of your private keys at all times. There are no manual transfers from your wallet to Oobit; funds are spent directly from your wallet balance.

Oobit is adding new wallet integrations every month, reinforcing its overall moat and broad user coverage across ecosystems.

Supported wallets include:

- MetaMask: the most widely used Ethereum wallet, trusted by millions of Web3 users

- Trust Wallet: 210M users globally (integrated Nov 2025), giving unmatched reach across chains

- Phantom: 15M+ Solana users (integrated Jan 2026), strong in the Solana ecosystem

- Binance Wallet: direct access to Binance’s massive trading and DeFi community

- Zerion: popular among DeFi power users for portfolio tracking and multi-chain access

- SafePal: hardware + software wallet solution, appealing to security-conscious users

Real-world traction. How Brazil and Argentina are spending crypto daily

Brazil (launched Oct 2025):

Oobit is actively expanding its operations in LATAM.

In October 2025, they opened a local office in Brazil and appointed Eduardo Prota, a FinTech veteran, to lead operations in the region. At pre-launch, Oobit onboarded about 50,000 new users.

Brazil is a book case study, being one of the top countries in the world adopting stablecoins. According to a survey conducted by Oobit, 91.8% of Brazilian crypto users hold stablecoins, with 85% mentioning they would like to spend them daily. But only 37% ever have.

According to Amram Adar, Co-Founder and CEO of Oobit, stablecoins are winning trust but losing the utility war in Brazil. Despite high stablecoin adoption, there is limited infrastructure for everyday spending at local outlets, and that’s where Oobit came in.

Oobit integrated the PIX payments platform in February, enabling 24/7, instant, and typically free money transfers and payments in the country.

Argentina (launched Mar 2026):

Oobit launched in Argentina in March 2026 amidst a broader financial system where stablecoins were playing a critical role in the fight against a depreciating local currency.

Argentina has one of the highest inflation rates in the world, with 2025 recording a rate of 31.50%. The government was adopting tight fiscal and monetary policies with projections suggesting a 20% rate in 2026.

Amidst the financial strain, Argentinians are adopting stablecoins to preserve value against the local currency depreciation. For Argentinians, stablecoins are a more reliable source of wealth and exchange medium.

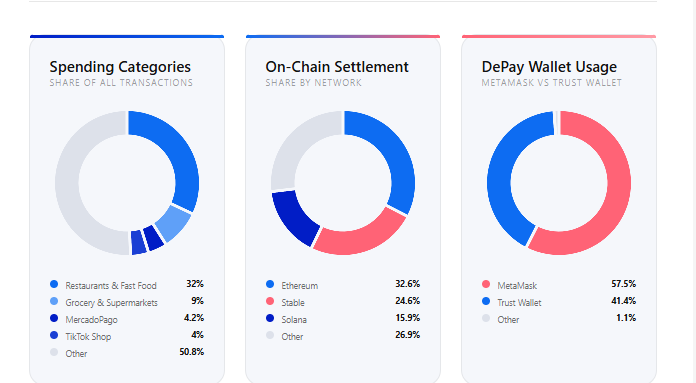

A study by Oobit revealed that 72% of all transactions made on the application were paid in USDT, closely matching the country’s stablecoin crypto trading activity at 70%. Argentinians are spending stablecoins at restaurants, supermarkets, and everyday merchants.

Oobit spending and settlement insights in Argentina

Food accounted for 41% of all user activity on Oobit in Argentina.

According to Amram Adar, Argentina is not a country to be convinced of stablecoin potential; all the market needed was a way to spend them.

Oobit also has active markets in the US (launched Dec 2025), South Korea, the Philippines ($38B annual remittance market), Singapore, the UAE, South Africa, and 100+ additional countries.

Beyond the card. Wallet-to-bank transfers and stablecoin payouts

Wallet-to-bank transfers (launched Feb 2026)

Oobit lets users sell crypto in non-custodial wallets for local currencies sent directly to bank accounts or supported e-wallets worldwide. The application supports over 25 cryptocurrencies, including BTC, USDT, ETH, and XRP, for conversion to local fiat.

There is no upper transfer limit on transfers, with the minimum being $10. Applicable fees are transparent and are shown upfront before you confirm the transfer.

Users can have the deposits made to their local accounts or to bank accounts in over 100 supported countries.

Supported local payment rails include: SEPA (Europe), ACH (US), SPEI (Mexico), PIX (Brazil), INSTAPAY (Philippines), Faster Payments (UK), BI FAST (Indonesia), IMPS (India), NIP (Nigeria), NEFT (India), Wire Transfer (US), and SWIFT.

Oobit Pay Peer-to-Peer crypto transfers with zero fees

Oobit Pay abstracts the complexity of blockchain transactions with an intuitive and user-friendly interface, making crypto transactions as simple as sending a text message.

Crypto transfers only require the recipient’s phone number or email address linked to their Oobit accounts. There are no wallet addresses, no intermediaries, and no transfer fees.

Conventional crypto transfers incur blockchain transaction fees ($1-50, depending on network) and carry the risk of address errors.

Supported cryptocurrencies include USDC, USDT, BNB, USDR, EURR, BTC, DOGE, ETH, SOL, TRX, XRP, XTZ, TON, VET, XAUT, LTC, XLM, TRUMP, ADA, BCH, and SHIB.

In the Philippines, Oobit Pays reportedly proceses $38 million in annual remittances.

Their mission is to connect the world’s wallets to real-world spending.

Oobit Bussiness

Oobit Business expands the platform into corporate finance, allowing companies to operate directly from their stablecoin treasury instead of relying on fragmented banking tools. Businesses can issue corporate Visa cards, pay vendors and contractors worldwide, manage spending, and move funds between stablecoins and bank accounts. By connecting blockchain treasury with payment rails like SEPA, ACH, and PIX, Oobit turns stablecoins from a passive asset into a fully operational financial stack for global companies.

| Feature | Oobit B2B stablecoin payouts | Legacy systems (Banks, SWIFT, PayPal) |

| Speed | Instant payouts | 1–5 business days, depending on banks and intermediaries |

| Cost | Flat 0.05% fee | Variable fees: 1–5% plus hidden FX charges |

| Minimum payment | Micropayments from $0.01 supported | Often restricted (e.g., $1–$10 minimums, or higher for wires) |

| Recipient setup | Only phone number or email linked to Oobit | Requires full bank details, account numbers, or PayPal IDs |

| Crypto wallet requirement | None, funds deposited directly into the Oobit account | Not applicable, but crypto transfers usually require wallets |

| Accessibility | Recipients without accounts get guided onboarding | Complex onboarding, KYC, and compliance checks |

| Spending funds | Instant access without bank delays | Funds may be held, delayed, or subject to withdrawal limits |

There is a wide application for Oobits B2B payouts feature: Creator platforms, freelance and gig networks, affiliate payouts, Web3 user rewards, fintech, and consumer applications.

Plug and Pay (B2B – for wallet providers):

Oobit Plug and Play B2B solution lets wallet providers embed a global Visa payment system in their applications using a few lines of code.

Oobit handles all the regulatory infrastructure, including card issuing, KYC, AML, and settlement. Unlike legacy systems, the payments infrastructure can go live in days, not months. At the same time, allow you all branding control.

Target businesses for Plug and Pay include crypto wallets, Web3 applications, stablecoin platforms, or exchanges expanding into payments.

Oobit business -Turning stablecoins into a corporate financial stack

Businesses can integrate the DePay infrastructure to create more utility for their cryptocurrency holdings.

With Oobit, the businesses can:

- Issue corporate Visa cards

- Pay vendors and contractors worldwide

- Manage spending

- Move funds between stablecoins and bank accounts.

By connecting blockchain treasury with payment rails like SEPA, ACH, and PIX, Oobit turns stablecoins from a passive asset into a fully operational financial stack for global companies.

Global availability, KYC, and supported regions

Oobit is a Singapore-registered entity and is currently pursuing a UAE license (Abu Dhabi office). US operations are powered by Bakkt’s regulated infrastructure, and are EU MiCA-compliant through the StablR partnership.

Oobit is available in over 100 other countries and expanding monthly. Some of these include Brazil, Singapore, the US, Argentina, the Philippines, South Korea, the UAE, and Nigeria.

KYC compliance is a standard requirement for all users for regulatory compliance and to prevent money laundering and fraud.

The virtual card is on the application, while the physical card is available for shipping on request. As stated earlier, there are no annual or holding fees on the card.

Oobit is, however, restricted in the following regions: Afghanistan, Iran, Iraq, Lebanon, Libya, Syria, Sudan, Belarus, Russia, Cuba, Nicaragua, Venezuela, the Central African Republic, Ethiopia, Mali, Somalia, and South Sudan

Oobit vs. traditional crypto cards: What’s actually different

Here is a quick comparison of Oobit and other conventional crypto cards:

| Feature | Oobit | Binance Web3 Wallet Card | MetaMask Card | Bleap Card |

| Custody model | Non-custodial until the point of sale | Custodial (pre-funding required via Binance app) | Non-custodial (funds stay in MetaMask until transaction) | Non-custodial (MPC-secured wallet, spend directly) |

| Wallet support | Multiple wallets via DePay | Proprietary Binance wallet only | MetaMask wallet only | Linked to the Bleap self-custodial wallet |

| Multi-chain support | ERC-20, TRC-20, BSC, SOL, Polygon | Limited (Binance ecosystem, BNB Chain focus) | ETH + stablecoins (mUSD, USDC, USDT, wETH, etc.) | BTC, ETH, SOL, stablecoins |

| Cashback | Up to 10% | Typically 1–5% (requires staking BNB or other tokens) | 1–3% depending on card tier (metal vs virtual) | 2% USDC cashback (capped at 10 USDC/month) |

| P2P transfers | Free & instant via phone number | Not available (exchange transfers only) | Not available | Global transfers possible, but fee-based |

| Settlement layer | DePay gasless on-chain settlement | Centralized internal ledger | On-chain (user pays gas fees) | On-chain, no FX fees, but the user pays gas |

Who is Oobit best suited for?

- Long-term holders who want to spend without selling on an exchange or giving up custody.

- DeFi-native users who live in MetaMask/Phantom/Trust and want IRL spending without leaving their wallet.

- Stablecoin holders, especially in LATAM (Brazil, Argentina), who use USDT as daily currency but couldn’t spend it at merchants, until now.

- Frequent travelers who need multi-currency spending at 150M merchants without FX friction.

- Freelancers and creators who receive crypto payments and want to spend instantly without off-ramping.

- P2P senders who frequently move crypto between contacts globally (remittances, splitting costs).

- Web3 applications that want to integrate a global payments infrastructure.

Final verdict

Your crypto should remain in your wallet until the moment you decide to spend it; that’s the principle Oobit has built around, extending self-custody to global Visa scale.

Unlike conventional crypto cards that rely on custodial intermediaries, Oobit operates as a payment ecosystem grounded in non-custodial design. This matters most for users unwilling to compromise on control but still needing everyday usability.

The technical foundation, DePay, enables gasless, multi-chain settlement through Visa rails, a genuine infrastructure advantage rather than a marketing claim. Incentives like 10% cashback are notable, but the more important signal is adoption: 50K+ daily users in Brazil and 72% of transactions in Argentina already flowing through USDT.

Oobit shift reframes the question for crypto holders: not whether to spend, but why assets should sit in someone else’s custody before they do. The custody gap is closed; Oobit demonstrates that self-custody and real-world payments can finally coexist at scale.

English (US)

English (US)